Comparison of Sites

- Home

- Incentives

- Location Support

- Comparison of Sites

Location support provided to facilitate and attract foreign

investment consists of foreign investment zones as prescribed by the Foreign

Investment Promotion Act , free trade zones as prescribed by the Act on Designation

and Management of Free Trade Zones , and free

economic zones as prescribed by the Special Act on Designation and Management . Among

these, foreign investment zones are further

classified into complex-type, individual-type, and service-type zones.

Specific details of location support available for foreign

investment, such as requirements, eligible businesses, and incentives (rental fees,

taxes, customs, cash) vary depending on the purpose of designation. It is

recommended that investors carefully review and analyze

investment locations, even for planned sites with seemingly simple procedures for

factory establishment, authorization, and permission.

Designation of Foreign Investment Zones

| Major Location Support | Designated Areas | Number | |

|---|---|---|---|

| Foreign investment zones | Complex-type | Cheonan, Daebul, Sacheon, Ochang, Gumi, Jangan 1, Inju, Dangdong, Jisa, Jangan 2, Dalseong, Oseong, Cheonan 5, Woljeon, Munmak, Jincheon-Sansu, Songsan 2, National Food (Iksan), Chungju, Gumi (parts), Pohang (parts), Iksan (parts), Changwon (parts), Mieum (parts), Songsan 2-1, Gwangyang-Sepung, Daejeon International, Eumseong-Seongbon, Songsan 2-2, Asan-Tangjung | 30 |

| Individual-type | Manufacturing (66), logistics (2), tourism (7), R&D (1) | 76 | |

| Service-type | Seoul (3) | 3 | |

| Gyeonggi-do foreign investment zones | Hyeongok, Poseung, Chupal, Eoyeon Hansan | 4 | |

| Free trade zones | Industrial site-type | Ulsan, Donghae, Gunsan, Daebul, Yulchon, Masan | 7 |

| Seaport · Airport-type | Port of Busan, Port of Pohang, Port of Pyeongtaek-Dangjin, Port of Incheon, Incheon International Airport | 6 | |

| Free economic zones | Incheon, Busan-Jinhae, Gwangyang Bay Area, Gyeonggi, Daegu-Gyeongbuk, Chungbuk, East Coast Area (Donghae), Gwangju, Ulsan | 9 | |

※ The designation of Saemangeum as a free economic zone was canceled on April 6, 2018, but the Saemangeum project is still underway in accordance with the Special Act on Saemangeum.

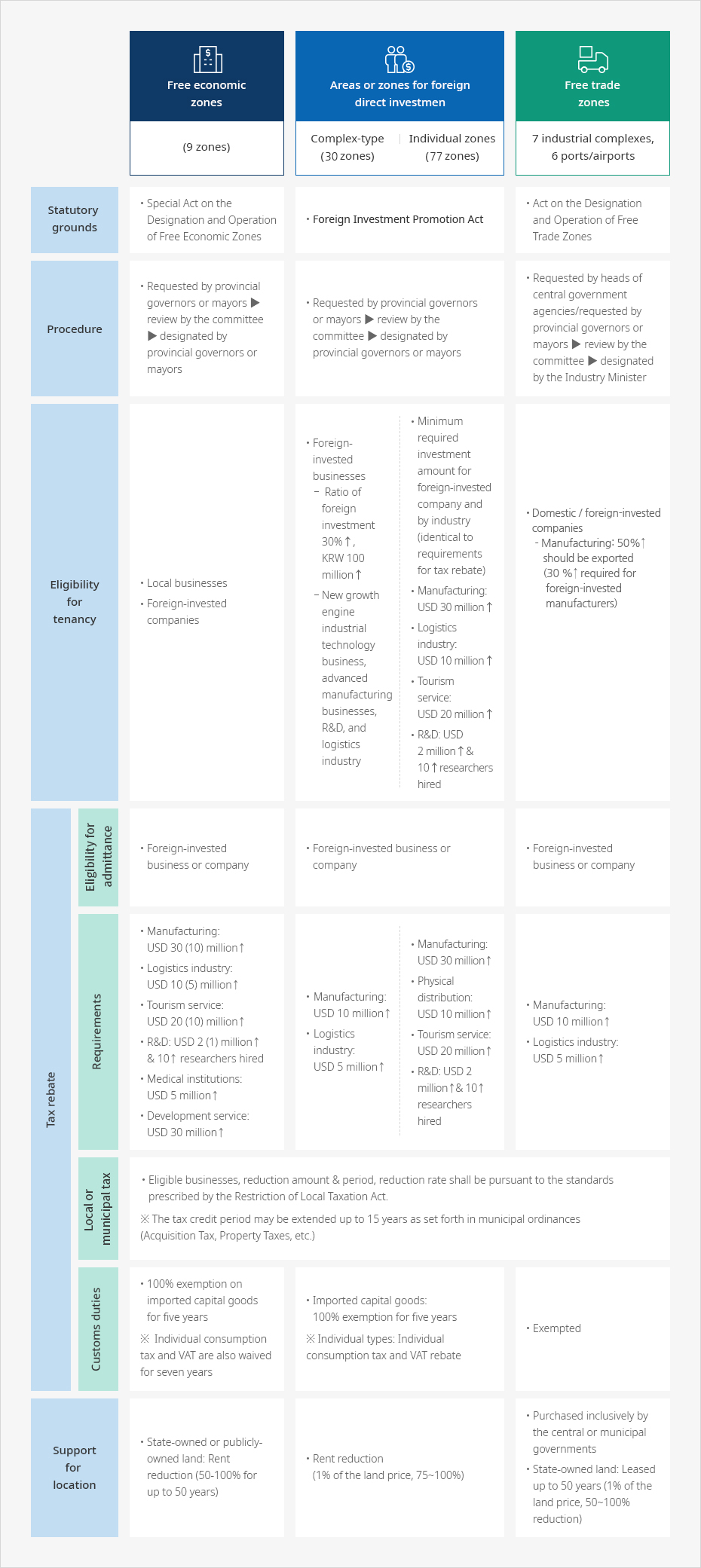

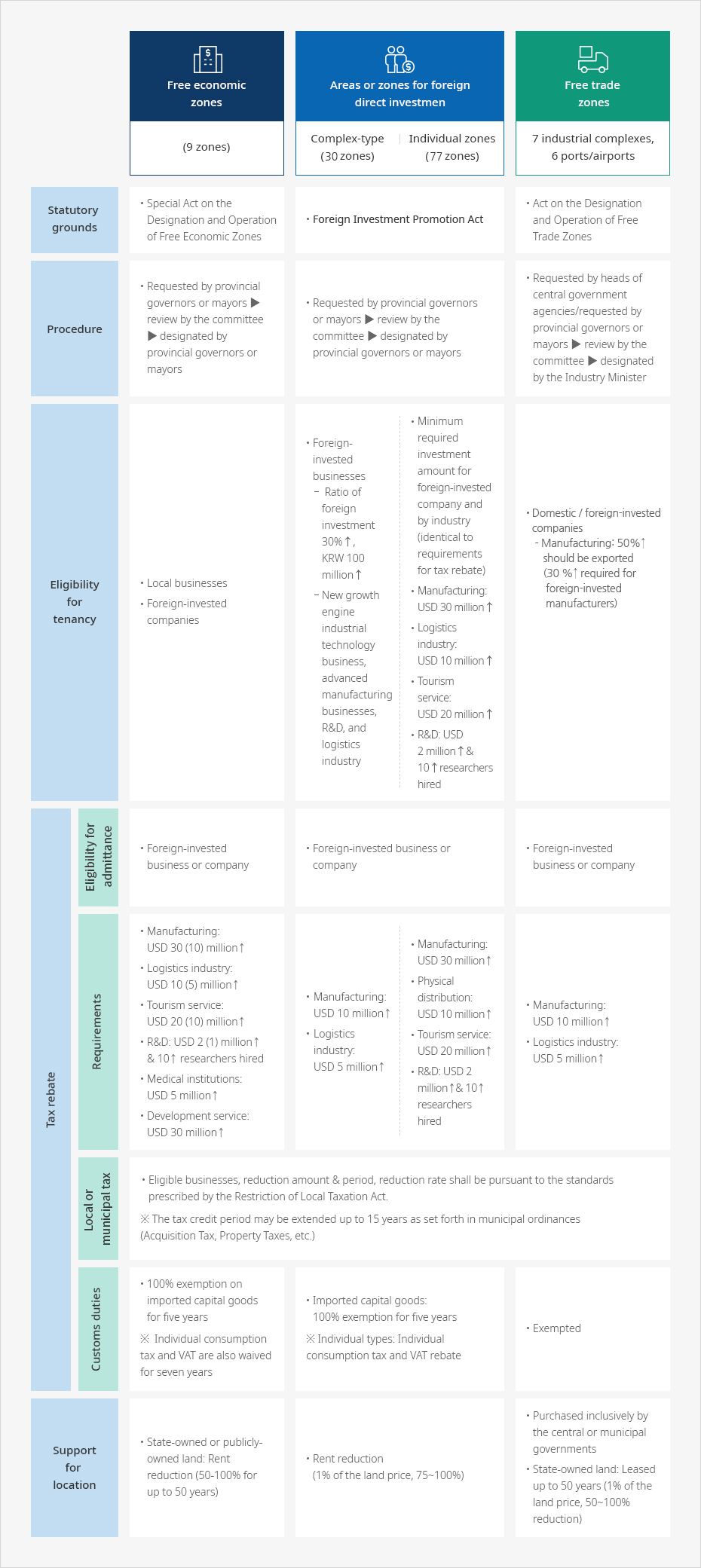

Comparison of Sites

| Free economic zones | Areas or zones for foreign direct investment | Free trade zones | |||

|---|---|---|---|---|---|

| 9 zones | Complex-type (30 zones) | Individual zones (77 zones) | 7 industrial complexes, 6 ports/airports | ||

| Statutory grounds | Special Act on the Designation and Operation of Free Economic Zones | Foreign Investment Promotion Act | Act on the Designation and Operation of Free Trade Zones | ||

| Procedure |

|

|

|

||

| Eligibility for tenancy |

|

Foreign-invested businesses

|

|

|

|

| Tax rebate | Eligibility for admittance | Foreign-invested business or company | Foreign-invested business or company | Foreign-invested business or company | |

| Requirements |

|

|

|

|

|

| Local or municipal tax | Eligible businesses, reduction amount & period, reduction rate shall be pursuant to the standards prescribed by the Restriction of Local Taxation Act. The tax credit period may be extended up to 15 years as set forth in municipal ordinances (Acquisition Tax, Property Taxes, etc.) | ||||

| Customs duties | 100% exemption on imported capital goods for five years Individual consumption tax and VAT are also waived for seven years | Imported capital goods: 100% exemption for five years Individual types: Individual consumption tax and VAT rebate | Exempted | ||

| Support for location | State-owned or publicly-owned land: Rent reduction (50-100% for up to 50 years) | Rent reduction (1% of the land price, 75~100%) |

|

||