The display industry has grown swiftly in recent years,

powered by rapid development of television and smartphone makers.

During this time, Korea has maintained its position as the largest

display manufacturer in the world. Thanks to growing demand

from television and its related industries, the world’s display

industry also quickly expanded until 2012. The following year,

however, it began to contract due to the global economic recession, shrinking an average of 4.5 percent annually from 2012 to

2015. As the Korean display industry is number one in the world,

it is highly affected by such changes in the global market.

From the 2000s, displays started to emerge as a new export-

driven industry, contributing to the country’s economic growth.

Exports grew exponentially, recording an average annual rate of

27.7 percent from 2006 to 2010. In 2013, however, the global

economic downturn and oversupply pushed export growth down

to -2.6 percent, and the figure has remained in the negatives until

2016.

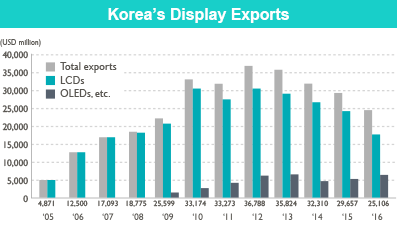

LCD (liquid crystal display) panel exports—the main driver of

the display industry—reached USD 18.2 billion in 2015, a 14

percent decline from the previous year, and fell further by 24.6

percent in 2016. Exports managed to recover slightly in the first

half of 2017, with a 11.7 percent year-on-year increase. In contrast, OLED (organic light-emitting diode) exports increased by

24.1 percent to USD 6.9 billion in 2016. With OLEDs being

applied to an increasing number of smartphone screens, the global demand for OLEDs has surged. OLED exports increased by

an annual average of 26.3 percent from 2014 to 2016, and continue to grow at about 20 percent this year. Thus, the OLED industry

is highly likely to lead the growth in exports for the entire industry.

Korea first emerged as the world’s largest display manufacturer in 2002, a title formerly held by Japan. By actively responding

to the changing environment through technological expertise and

bold facility investments, Korea quickly succeeded in taking the

No. 1 spot in the global flat panel display market. Despite the

recent slowdown in production and exports caused by the global

economic recession and oversupply, Korea still holds the largest

share of the global display market thanks to its industrial competitiveness.

In an effort to secure production hubs targeting China’s local

market and other export destinations, Korean companies have

initiated mass production at their LCD panel factories in China

(Samsung in Suzhou, LG in Guangzhou) in 2013. But the greatest obstacle for Korean display exports is the rise of China, as the

country is producing its own products and relying less on Korean

displays. This trend is expected to continue for the foreseeable

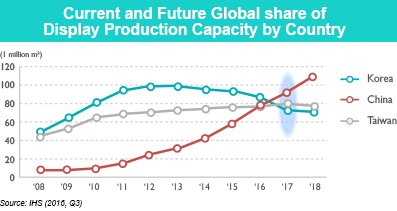

future. Since China started to focus on expanding its display

industry, it is expected to overtake Korea in terms of LCD production capacity in 2017. China’s LCD production capacity was

10.5 percent of the global total in 2013, but is expected to rise to

35.1 percent in 2017, and 40.1 percent in 2018.

A noteworthy change in China is that local companies are

actively investing in 10.5th-generation panels, a field Korea has

yet to invest in. China’s BOE Technology Group has commenced construction of a 10.5th-generation LCD panel produc-

tion line in 2015, and expects to gain a competitive edge for

ultra-large TV screens. In the second quarter of 2018, the company aims to begin operations at the 10.5th-generation factory,

where it plans to make large panels for 65-inch or wider TV

screens. China Star Optoelectronics Technology (CSOT), a subsidiary of large home appliances maker TCL Corporation, has

also decided to invest in the world’s largest 11th-generation LCD

panel production line and begin production in 2019. Other Chinese companies

such as HKC Electronics and CEC Panda

Crystal Technology have started to invest in 11th-generation

facilities and equipment. As such, Korea and China are soon

expected to compete on an equal footing in the global LCD

industry.

In contrast, for OLEDs, which are currently emerging as a new

type of display for the post-LCD era, Korean companies have

already secured a dominant 95 percent of the global market. As

such, it is very likely that Korea will continue to lead the global

display industry for some time. Korean panel companies have

started to replace their main LCD products with OLEDs, and

have established plans to focus their investments on related technology.

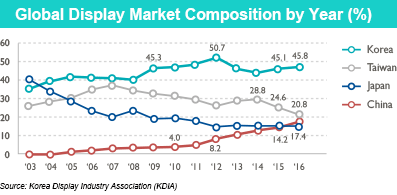

First, the scale of Korea’s domestic display market is relatively

small, and approximately 84 percent of all its manufactured

products are exported. Estimates for 2016 show that exports

account for 91 percent of LCD and 70 percent of OLED products

made in Korea. As the rapid rise in OLED exports partially offset

the poor performance in LCD exports, the emergence of the new

product is confirming the strengths of displays as an exports

industry.

Second, the fact that the world’s largest and second largest display manufacturers are based in Korea is probably the greatest advantage of the country’s display industry. With the world’s two largest display manufacturers—Samsung Display and LG Display—being based in Korea, the domestic display industry’s highly competitive structure has been driving development. It is also contributing to the establishment of a favorable business environment. The competition between the two companies has accelerated investment in new product and technological development, thus contributing to the industry’s continuous growth.

Third, the presence of a strong network of upstream and downstream industries in the country offers companies the stability to carry out production activities and strengthens their competitiveness. Supported by a network of smartphone, telvision, home appliances, automotive and other highly-developed industries with a demand for displays, as well as the rapid development of key parts and display equipment fueled by the panel industry’s high level of competitiveness, Korea boasts an optimum environment. Challenges remain, however, including the need to strengthen the country’s technological prowess in display materials and equipment. While the rate of domestically produced materials and equipment has radically improved, the country still struggles to develop technologies for key materials and equipment, relying heavily on imports from Japan and other technologically-advanced countries.

With global display markets projected to witness modest

growth until 2020, OLED products are expected to drive growth

in the entire industry due to the soaring demand for OLED

screens for smartphones. Currently accounting for 95 percent of

the newly emerging global OLED market, Korea is expected to

enjoy the fruits of the global surge in demand for some time.

This is because it will take at least several years for its competitors in countries such as Japan or China to be able to mass produce OLEDs.

In 2015, OLED panels accounted for 10 percent of the global

display market, but the figure is projected to reach 25 percent by

2022. Currently, most OLED displays are used as smartphone

and TV screens, but the market is expected to expand greatly as

technology evolves to enable the production of flexible and

transparent OLED displays.

On the other hand, the share of LCDs is expected to continue

to decline, as the expansion of China’s LCD output acts as a

major obstacle to growth. While China is the world’s biggest

market for LCD panels, Chinese companies account for over 70

percent of the local TV market. Therefore, as the country continues to raise its LCD output, it seems there will be increasingly

fewer opportunities for Korean companies to supply LCDs to

Chinese TV companies.

In conclusion, although Korea’s display industry is expected to

encounter difficulties due to competition with China in LCDs, if

OLED panels start becoming a popular option for TV screens

and demand for OLEDs rises in the field of new convergence

technologies, Korea is expected to enjoy an even greater number

of opportunities for growth. As OLED markets continue to

expand, rival countries such as China, Japan and Taiwan will

also expand their investments. But because Korea has a clear

competitive advantage in mass production capacity and product

development over its rivals, it is expected to maintain a significant lead over its three key competitors until 2020.

The shift in the global industrial paradigm during the fourth

industrial revolution is expected to create new opportunities in

the display industry, as the demand for displays increases not

only for flexible screens, but also for wearable devices, smart

cars and smart homes. Should Korea’s display industry focus on

expanding OLED markets and accumulating related technology,

it is expected to strengthen its global dominance even in the new

markets of the future.

* The opinions expressed in

this article are the author's own and

do not reflect the view of KOTRA.