- Home

- Industries

- Industry News

- Industry Focus

Industry Focus

Korea’s cosmetics brands are diversifying their strategies to appeal to a wider audience, most notably in China.

The Future driver of exports

In the past, Korea’s cosmetics export was less than half that of Japan’s. Since 2009, however, the Korean Wave helped drive up demand for Korean cosmetics, catapulting the country’s brands into the spotlight. Namely, the demand for such products has mainly come from Asia. Such an increase in exports serves as proof that the demand for “made in Korea” products is growing much faster that of its Japanese counterparts. In short, Korea is revolutionizing the environment of the Asian cosmetic industry.

With the Korean Wave making a splash throughout Asia, Korean celebrities and content gained great popularity. The country’s products also became highly sought out along with this phenomenon. As a result, more and more tourists are visiting Korea to not just travel, but to shop for Korean cosmetics.

Size of global cosmetics market and export volume per country

(In USD million)

| 2004 | 2009 | 2014 | 04-09 CAGR | 09-14 CAGR | 04-14 CAGR | |

|---|---|---|---|---|---|---|

| Size of global cosmetics market | 275,852 | 359,095 | 464,518 | 5.4% | 5.3% | 5.3% |

| Export volume per country | ||||||

| EU | 9,382 | 15,426 | 20,252 | 10.5% | 5.6% | 8.0% |

| France | 3,777 | 5,888 | 7,753 | 9.3% | 5.7% | 7.5% |

| Italy | 825 | 1,086 | 1,549 | 5.7% | 7.4% | 6.5% |

| UK | 1,027 | 1,476 | 2,061 | 7.5% | 6.9% | 7.2% |

| Germany | 1,530 | 2,775 | 3,107 | 12.6% | 2.3% | 7.3% |

| US | 1,810 | 2,779 | 3,944 | 9.0% | 7.3% | 8.1% |

| Japan | 563 | 965 | 1,174 | 11.4% | 4.0% | 7.6% |

| Korea | 164 | 373 | 1,598 | 17.9% | 33.8% | 25.6% |

Future prospects

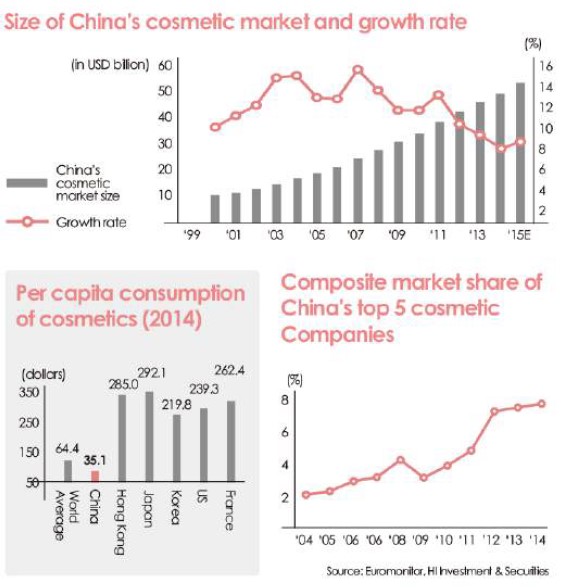

China’s per capita cosmetics consumption is less than 20 percent that of Korea. And yet, China ranks second following the US in terms of market size. As China’s income levels will rise in the future, the Chinese market has become a competitive playing field for global cosmetic companies. Against this backdrop, Japan has already lost its ground to Korea while Chinese demand for Korea’s cosmetics is growing exponentially.

In the midst of such fierce competition, China’s local cosmetics companies are growing fast, accounting for 20 to 30 percent of the country’s cosmetic market share. According to data released by Euromonitor, the total market share of the top five Chinese companies (namely Shanghai Jahwa, Jala, Jiangsu longliqi, Shanghai inoherb and Proya) increased from 2.1 percent in 2004 to 6.8 percent in 2014. With the exception of Shanghai Shuang Mei and Herborist, most of the Chinese local brands were low and medium-end brands rapidly expanding their market share.

In contrast, data shows that most of the international brands produced medium or high-end products. Thus, Chinese companies will not pose an immediate threat to Korean or other international companies unless they begin to expand their market in the premium cosmetic sector, which will take more time to develop than low-end products.

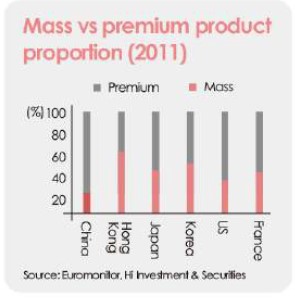

In the future, the premium cosmetics sector is expected to enjoy the fastest growth in the Chinese cosmetic market. As of 2011, the premium segment accounted for 19 percent of the country’s cosmetic market, considerably lower than Korea’s 48.7 percent, Japan’s 42.5 percent, the United States’ 33 percent, France’s 40.9, and Hong Kong’s 61 percent. But China’s figure is a huge step up from its previous numbers, as the premium cosmetics sectors only made up 9 percent in 1998. Like Korea, analysts expect China to also experience growth in its premium sector thanks to increased income level and aging population, among other factors. This sector of the Chinese cosmetic market is currently dominated by international brands. As explained before, Chinese companies have not caught up with their international counterparts in premium lines yet.

In addition, the recent market trends are indicating that Chinese consumers prefer premium brands. According to a recent data released by KOTRA (excluding for e-commerce data), only medium and high-end products saw an increase in their department store sales as of the first quarter of 2015, while sales of low and medium-end products decreased. Compared to several years ago, consumption on imported cosmetic products has grown much faster, surging in 2014 and showing strong growth to date. It is noteworthy that most of the consumer spending was made on expensive international brands.

Strategies implemented by Korean companies

1. Amore Pacific

(1) Company prospects

Despite concerns over China’s economic slowdown, the cosmetic industry still has a great potential for growth since a number of brands has recently emerged in the Chinese market. Last year alone, more than 200 brands appeared in the Chinese market. This trend is continuing with parts and distribution companies seeking to enter the cosmetic business to secure the growing number of consumers. In terms of age, young consumers are increasing their expenditure on cosmetics, demonstrating a stronger purchasing power. Those born in the 1990s accounted for 15 percent of total consumption in 2012 and the figure is likely to increase to 35 percent by 2020—a major reason why Amore Pacific considers China to be a promising future market.

(2) Objective for 2020

Amore Pacific aims to achieve a gross sales record of KRW 12 trillion (USD 10.2 billion) by 2020. Its Chinese branch, in particular, seeks to achieve a sales record of over KRW 3 trillion (USD 2.6 billion). Under such circumstances, Amore Pacific is planning to increase the number of employees at Chinese branch from 40 to 100 by 2020, as well as designate more personnel into R&D projects. In order to maintain growth in China, the company is also planning to expand its brand portfolio, release products tailored to the needs of Chinese consumers, and quickly respond to customers through digital platforms.

(3) Opportunities for growth

In response to the latest trends, the company’s sales strategies are becoming more diverse. On this note, Amore Pacific has gained a strong foothold in Asia thanks to its competitive brand portfolio, boasting a wide range of products from “masstige” products (a combination of mass and prestige) such as Innisfree and Etude House to luxury products like Sulwhasoo. Moreover, each brand has its own distinct theme like herbal medicine, flowers and nature.

The case study of global cosmetic firms offers quick and useful lessons. For example, L’oréal and Estée Lauder are constantly expanding their brand, while Mary Kay, Elizabeth Arden, and Shiseido are showing lackluster performance compared to before. There is one remarkable difference that distinguishes the former group from the latter—a diversified portfolio.

Cosmetic consumers have specific individual needs. Companies trying to satisfy the various needs of consumers with just one brand will inevitably face many limits. As such, we expect Amore Pacific to cater to Chinese consumers through different approaches.

2. LG Household and Health Care

(1) Business portfolio

One positive element for the company’s future is the cosmetic industry’s huge potential for growth. On this note, LG Household and Health Care has gained a competitive edge in this sector and is benefitting from increased sales in the Chinese market. The company’s performance in the daily supplies and beverage businesses is rather lackluster, but its cosmetics business is doing incredibly well. The profit proportion of cosmetic businesses will gradually increase from 50 percent in 2014 to 53 percent in 2015.

Amore Pacific thus has come up with a new slogan called “Global Beauty & Personal Care Company” in order to focus on expanding its cosmetic businesses. China’s strong demand for Korean cosmetics and other favorable market conditions will lead to the industry’s rapid growth.

(2) High-end cosmetic products to attract Chinese consumers

LG Household and Health Care’s representative high-end brand, Hu, has gained much popularity among Chinese consumers recently and recorded high sales, particularly at duty-free stores. The company is making more of an effort to expand its distribution channels in China to swiftly respond to increasing demands. As part of the efforts to progressively launch brands and expand distribution channels, the brand Hu increased its number of branches from 89 to 124, opened its online store at Tmall Global, and launched its oriental herbal shampoo ‘Rien’. Furthermore, product sales of Sum, another one of its brands, grew two-fold at duty-free shops in 2015 and it continues to record strong numbers. Against this backdrop, both Sum and Hu are expected to become beloved premium brands in China this year.

Son Hyo-ju

Researcher, HI Investment & Securities

hjson@hi-ib.com

The above article does not necessarily reflect the views or position of KOTRA.